ABC Analysis Logistics

ABC analysis in logistics – Definition

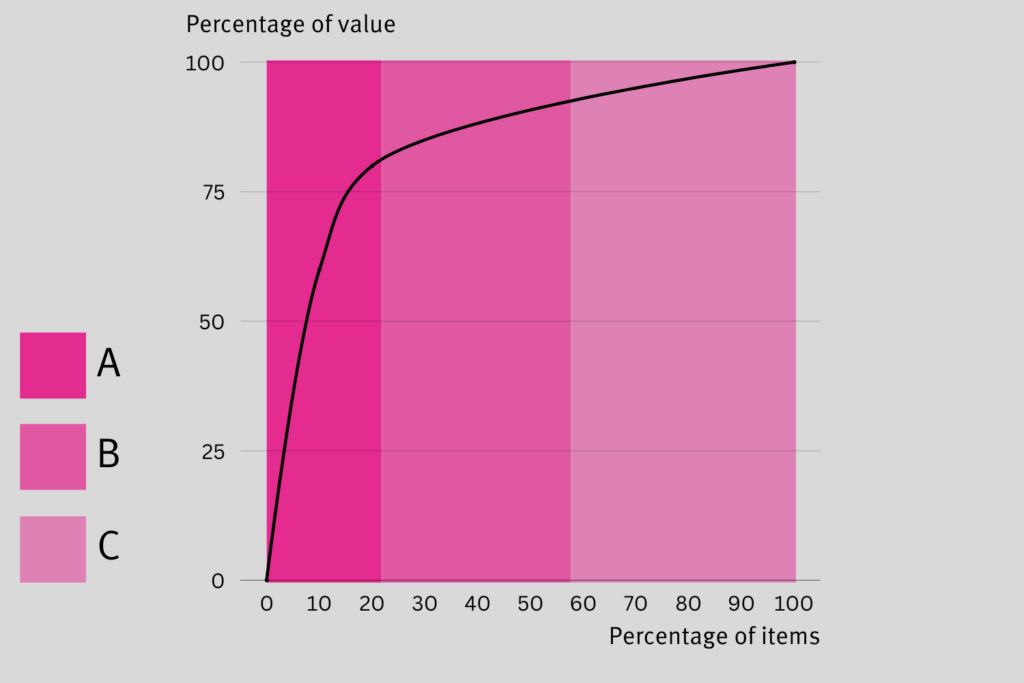

The ABC analysis is a method to control the goods distribution within a warehouse. Therefore, it concerns the prioritisation and organisation of the goods placement within the warehouse and of the procurement of goods. However, the decisive factors here are the relevancy and the economic importance of an article, not the amount. For that, goods can be sorted into three groups.

Classification based on stock

A goods

A goods are the most important goods group. As a rule of thumb, they account for approximately 20% of the warehouse stock in terms of quantity, but account for a high proportion of the generated turnover at about 80%. Therefore, A goods should always be stored where they are easily accessible (e.g., in the high rack, on the lowest levels) and a sufficient stock should always be available.

B goods

B goods are in the middle of the pack when it comes to both the quantity and the value proportion. Here, you do not need to be as precise with the stock control. B goods are stored higher up than A goods most of the time.

C goods

Even though C goods account for a relatively large proportion of the quantity, their proportion of value is very low. These goods are not requested that often, which is why it is not necessary to keep such large stocks of them.

Calculation of the turnover rate

Based on unit costs

If you want to calculate the transshipment frequency of goods based on unit costs, you need to consider all costs that arise for the goods. Therefore, the importance with which the goods are procured increases with the costs of the goods.

Based on total value

Here, the quantities of the stock that are currently available in the warehouse are used for the calculation. As the stock is, of course, always changing, regular recalculation is necessary.

Based on demand

This method is the most common version of warehouse stock planning. The demand for a good and its value are the calculation basis. That way, goods that have a high value but are only rarely requested do not become A goods.

Practical example for ABC Analysis

To illustrate the topic, the ABC analysis can be explained with the following example. A company for cosmetics products has 100 pallet store places in the warehouse and has a yearly turnover of 1 million euros. The “Basic” product range consists of hand cream, body lotion, shower gel and shampoo and takes up 20 pallet store places in the warehouse. With this product range, the cosmetics company has a turnover of €800,000 per year. The “Basic” product range are A goods. Another 35 pallet store places are required for other products that are less in demand (B goods) and the remaining 45 pallet store places are used for many small niche products that only make up a small part of the turnover and are not ordered very often (C goods).

See also:

Free-Flowing Bulk Material (FFBM) Free-flowing bulk material is a term used in freight transport and refers to goods without a fixed geometrically defined shape< [...] Dangerous Goods The term dangerous goods refers to materials and goods that can pose a threat during the transport process. These dangerous goods are d [...]